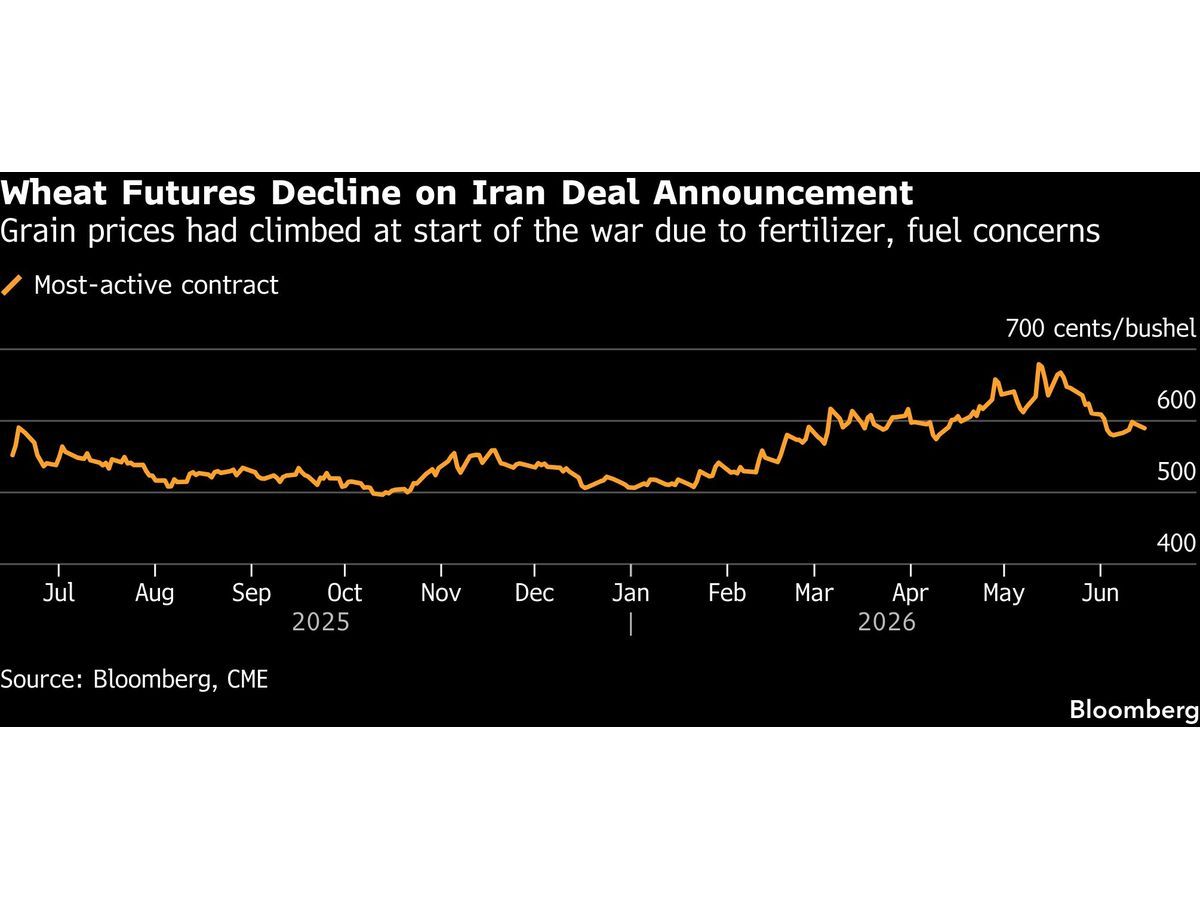

Grain Futures Decline as Potential Hormuz Reopening Promises Relief on Farm Inputs

Global grain markets are reacting swiftly to shifting geopolitical winds, with futures on the Chicago Board of Trade experiencing a notable decline. This downward trend is primarily driven by the potential reopening of the Strait of Hormuz, one of the world's most critical maritime chokepoints. For the agricultural sector, the normalization of traffic through this route signals a much-needed easing of the severe input supply shocks that have burdened farm budgets in recent months.

The strategic importance of the Strait extends far beyond crude oil; it is a vital artery for the global trade of liquefied natural gas (LNG) and key agricultural chemicals produced in the Middle East. For European farmers, previous disruptions meant significantly inflated costs for nitrogen-based fertilizers, agrochemicals, and fuel. Restoring reliable maritime logistics through this corridor is expected to stabilize these essential farm inputs, potentially lowering operational expenses as agricultural enterprises secure supplies for upcoming field operations.

However, this anticipated relief on the cost side comes with immediate consequences for agricultural commodity pricing. Traders have quickly priced in the reduced geopolitical risk and the prospect of cheaper crop production, triggering a sell-off in wheat, corn, and soybean futures. European grain producers, who are already navigating complex local markets and shifting trade dynamics, now face the reality of a softer global pricing environment for their upcoming harvests.

The broader implications for the supply chain are substantial. A smoother flow of agricultural inputs helps dampen global food inflation, which had spiked due to compounded logistical bottlenecks and soaring production costs. For agritech companies, cooperatives, and supply chain managers across Europe, stabilized input markets reduce the necessity for aggressive stockpiling, allowing for more predictable procurement cycles and improved cash flow stability.

What this means for the market: While the prospect of cheaper fertilizers and diesel is a welcome development for farm profitability, the simultaneous drop in crop prices requires careful margin calculation. Agronomists and farm managers should weigh the benefits of locking in lower input costs now against the need to strategically hedge their grain sales to protect against further downward price pressure.

— agronom.work editorial team